US prepares to strike Iran

23 February 2026 — Will the US launch a strike on Iran? Why is the World Uncertainty Index at record highs? What does the US Supreme Court decision mean for Donald Trump’s tariff agenda? What do the latest jobless numbers tell us about the economy? What are the implications of the recent political upheaval in Ekurhuleni?

Welcome to the weekly Risk Alert from the Centre for Risk Analysis — 23 February 2026

US prepares to strike Iran

In terms of air and sea power, the United States (US) is assembling its largest military force in the Middle East since the invasion of Iraq in 2003. According to defence specialist Robert Pape, around half of the US deployable air power is now being concentrated in the Middle East. He adds: “Never has the US deployed this much force against a potential enemy and not launched strikes.”

In response, the price of Brent crude hit its highest level in six months, at almost $72 per barrel. On Friday, amidst ongoing talks between the US and Iran, President Donald Trump said he was considering a limited military strike against Iran, indicating he considered around 10 to 15 days the “maximum” he would allow for negotiations on Iran’s nuclear programme to be concluded, or “bad things will happen”.

Iranian retaliation against a US strike, should it occur, is likely to target US and Israeli military and civilian assets in the region. In the event, Iran is also expected to try to close off the Strait of Hormuz, through which around 20 million barrels of petroleum products flow per day. This amounts to approximately a fifth of total global petroleum liquids consumption.

South Africa is especially vulnerable to rising international oil and fuel prices. With much of its domestic refining capacity having been shut down, South Africa can only meet around 30%-40% of its refined fuel needs, meaning between 60% and 70% has to be imported. Should the US and Iran enter open conflict, South Africa could feel the shock to global supply acutely, directly via fuel price increases and in the longer term through elevated inflation.

The African National Congress (ANC) and a succession of ANC-led governments have long maintained warm relations with the Iranian government, which the US designated a state sponsor of terror in 1984. This has led to rising diplomatic friction between Pretoria and Washington DC, which any military conflict between the US and Iran would escalate.

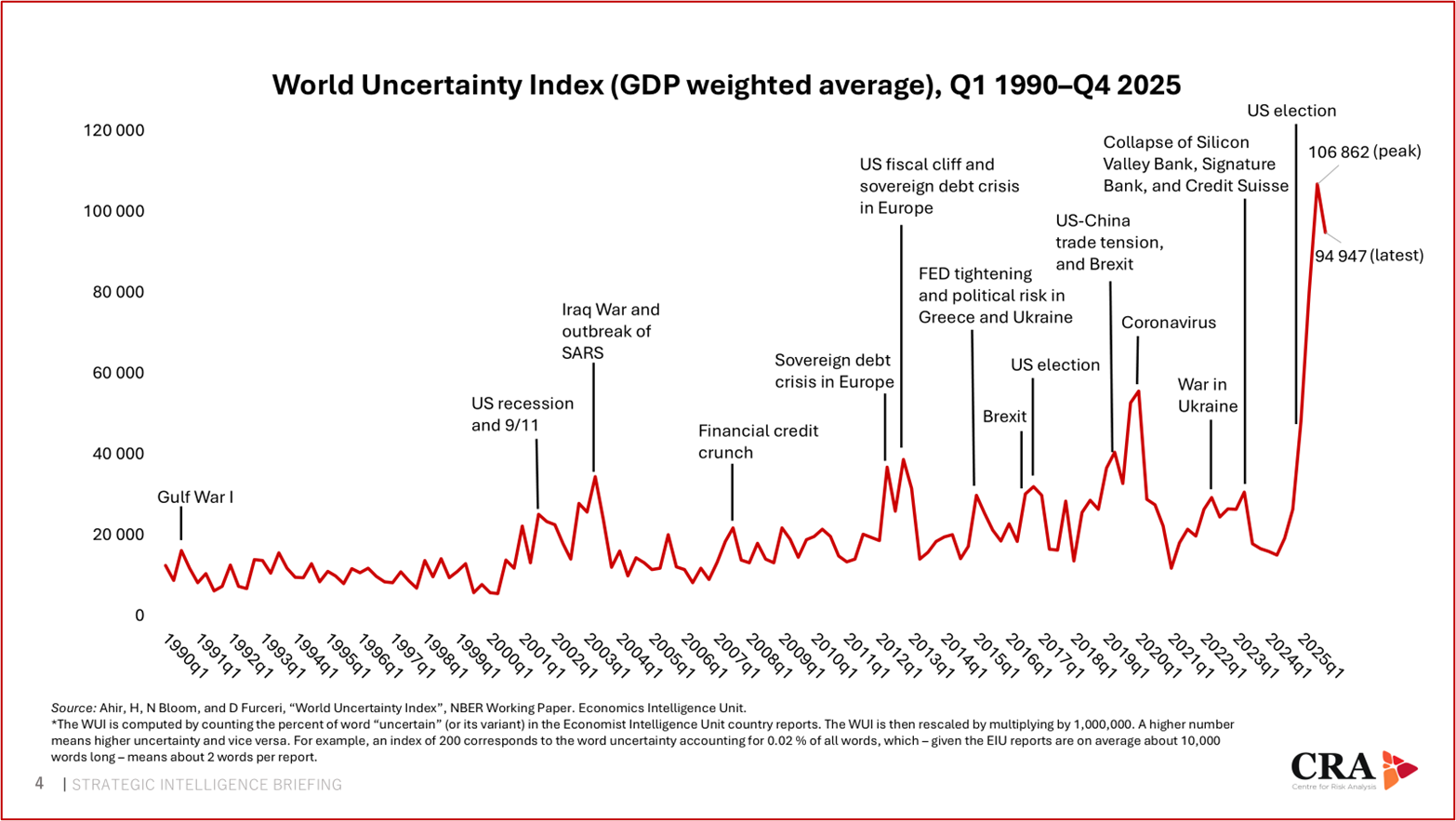

World Uncertainty Index at record high levels

The escalation in US-Iran tensions and legal upheaval surrounding US trade tariffs form part of a broader global environment defined by compounding geopolitical risks.

This is reflected in the World Uncertainty Index (WUI), which reached a historic all-time high of 106,862 in the third quarter of 2025, according to data from the Federal Reserve Bank of St Louis in Missouri. While it receded slightly in the fourth quarter — to 94,947 — it remains elevated far above the historical norm. In a time series stretching back to 1990, the previous highest reading was 55,685 in Q1 2020, during the first months of the Covid-19 pandemic.

Unlike previous shocks, typically driven by a single dominant driver — a terrorist attack, a financial system failure, or a pandemic — today’s environment is characterised by multiple high-impact events all generating uncertainty simultaneously.

They include trade fragmentation, major power rivalry, high sovereign debt levels, overlapping regional conflicts, a disruptive technological innovation in the form of artificial intelligence, and institutional stress in advanced economies. It is also worth noting that the rapid recent rise in uncertainty coincides with the US presidential elections of 2024 and the beginning of the second Trump term in January 2025.

However, despite record-high uncertainty, major equity indices remain positive year-to-date. Liquidity from earlier stimulus cycles continues to support asset prices, while optimism remains concentrated in technology and artificial intelligence.

By contrast, currency and commodity markets are sending mixed signals, leaning towards caution. The US Dollar Index has weakened by almost 10 points year-on-year, registering at 98 last Friday. Gold has surged, peaking above $5,500 in early 2026. Silver has almost tripled over the past year, and oil prices are trending higher in anticipation of a possible supply shock.

These moves are consistent with a classic “fear trade” and suggest that sophisticated market participants are hedging against geopolitical and macroeconomic shocks rather than dismissing them.

South Africa remains highly exposed to global macro developments due to its commodity-heavy economy, reliance on exports — especially to China, Europe and the US, Rand sensitivity to risk sentiment, and vulnerability to energy/import inflation.

South Africa’s business owners should plan for choppy conditions, including higher input costs, supply chain disruptions, and slower global economic growth that could reduce the demand for commodities.

SCOTUS tariff ruling

Adding to the uncertainty, the US Supreme Court ruled on a 6-3 vote on Friday, 20 February, that Mr Trump had exceeded his legal authority when he imposed sweeping tariffs using the 1977 International Emergency Economic Powers Act (IEEPA). The ruling reaffirmed the US Congress’s constitutional control over taxation and duties.

US importers now have a legal basis to demand refunds, according to Reuters, estimated by some sources at up to $175 billion (R2.9 trillion). The court stated that refunding billions from tariff collections was likely to be “a mess” but might be required, without making an explicit decision.

Despite the ruling, tariffs will not return to pre-2025 levels. Treasury Secretary Scott Bessent told the Economic Club of Dallas, Texas that using alternatives to the IEEPA would result in “virtually unchanged” 2026 tariff revenue for the US. Those alternatives include Sections 122 and 301 of the Trade Act of 1974 and Section 232 of the Trade Expansion Act of 1962.

As matters stand, Mr Trump revoked the IEEPA tariffs via an executive order on 20 February and replaced them with alternatives, including a new global tariff set first at 10% and then apparently raised (via a post on Truth Social on 21 February) to 15%. This replaces the 30% global tariff previously imposed on South Africa and comes into effect from 24 February 2026. It is scheduled to last for up to 150 days unless modified or terminated earlier by Congress. Separately, tariffs imposed since 2025 on steel products (50%), aluminium products (25%), and automobiles and automotive parts (25%) under Section 232 will remain.

Gauteng and KZN shed jobs, Western Cape gains

The latest Quarterly Labour Force Survey numbers show that South Africa’s jobless rate has declined from 31.9% in Q3 2025 to 31.4% in Q4 2025. While that is the lowest it has been in the last five years, it is still above the pre-Covid rate of 29.1%, recorded in Q4 2019. On the expanded definition, which includes discouraged job seekers, the unemployment rate was 42.1%, down slightly from the 42.4% recorded the previous quarter.

From a provincial point of view, two provinces that are vital for South Africa’s overall economic prospects, Gauteng and KwaZulu-Natal, shed 54,000 and 41,000 jobs, respectively. These two provinces are home to around 45% of the country’s population. Given its industrial heft, Gauteng’s performance is especially concerning.

By contrast, the Western Cape recorded the lowest provincial unemployment rate, of 18.1%, as well as adding the most jobs of any province: 93,000 quarter-on-quarter, almost as many as Gauteng and KZN lost.

Ekurhuleni warning signals for Gauteng politics

Last week the mayor of Ekurhuleni, Nkosindiphile Xhakaza of the African National Congress (ANC), shook up his mayoral committee in a late-night reshuffle.

Having been offered two committee positions, two less than the four it held previously, the Economic Freedom Fighters (EFF) rejected the reshuffle, joined by ActionSA. The EFF announced it was pulling out of the governing coalition, while ActionSA national chairperson Michael Beaumont said his party did not see this as “a government we want to find ourselves accountable with”.

The Ekurhuleni governing coalition government consisted of the ANC, EFF, ActionSA and Patriotic Alliance, with 136 of the 224 total council seats. Without the EFF’s 31 seats, the governing coalition will be reduced to 105 seats and will no longer have a majority, making the mayor vulnerable to motions of no confidence and placing at risk his coalition’s ability to pass a budget.

Amidst other threats, EFF leader Julius Malema said his party would reconsider its support for the ANC at provincial level, where the premier, Panyaza Lesufi, governs through a minority government thanks to tacit EFF support.

The implication is that disturbances in the Ekurhuleni city council could lead to disruptions in other councils and at the provincial level in Gauteng. Under such pressure, it is plausible that the ANC will fold and give the EFF what it demands. In this conflict, the interests of residents and voters are irrelevant.